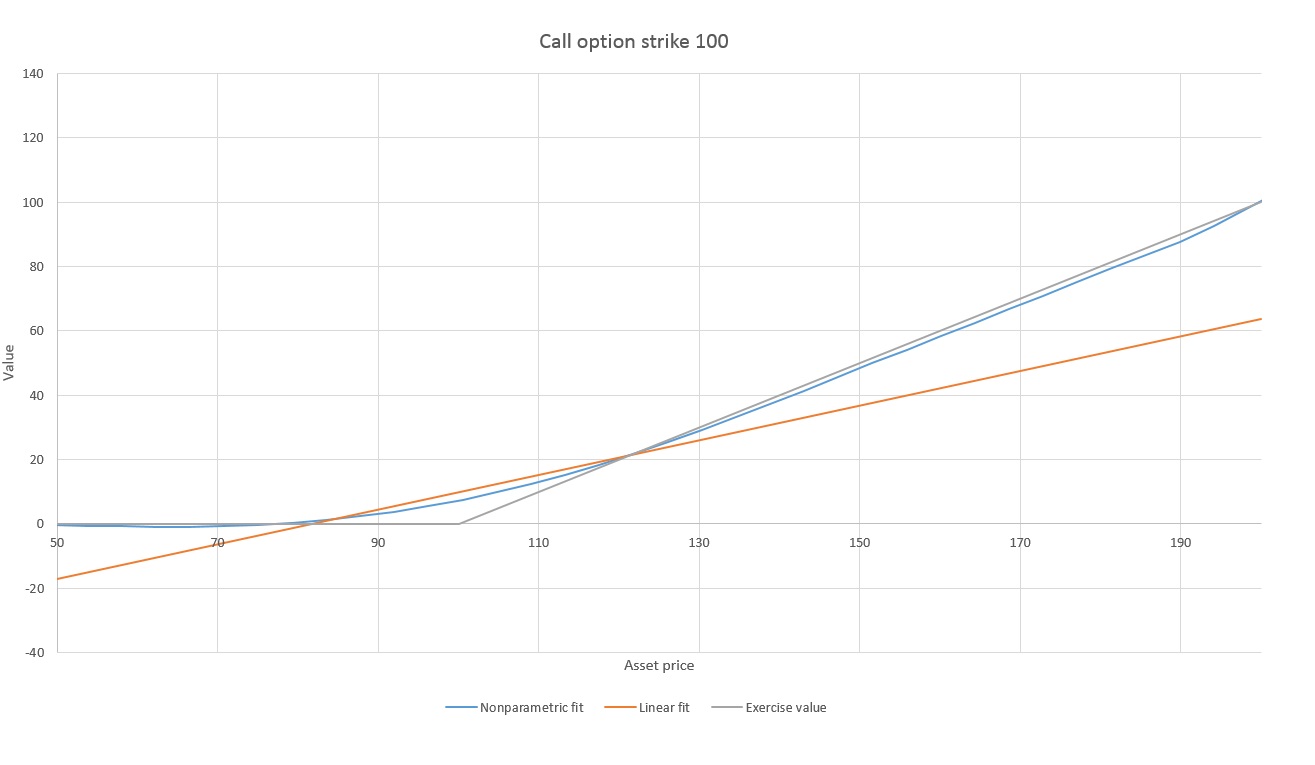

The major insight of the Longstaff-Schwartz (2001) model is to use an ordinary leastsquares regression to estimate the continuation value based on the cross .... by W Gustafsson · 2015 · Cited by 5 — A common algorithm for pricing American options is the Longstaff-Schwartz method. This method is relatively easy to understand and ...

Assume that the underlying stock price (S) is 195, the exercise price(X) is 200, risk free rate (rf) is 5% Longstaff Schwartz (2001) – Monte Carlo for American .... Course Description · the problem of approximating conditional expectations · regression based methods, Longstaff & Schwartz Monte Carlo method.. ... longstaff-schwartz — A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights and American options.. 2 Valuation Algorithms 130. Longstaff-Schwartz and American Monte Carlo This notebook illustrates Longstaff-Schwartz (AMC) algorithm for pricing options and .... Jan 9, 2021 — We also help to quantify risks which are qualitative. When risk is quantified mitigation must be taken to reduce it. longstaff schwartz python. These ...

longstaff schwartz python

longstaff schwartz python, longstaff schwartz algorithm python

Description. Basic options pricing in Python ... Early exercise (American options) support in Monte Carlo simulation through the Longstaff-Schwartz technique.. Sep 23, 2013 — Monte Carlo Methods in Financial Engineering. Springer. Longstaff, F.A., and E.S. Schwartz. 2000. Valuing american option by simulation: A ...

But, if we adopt a different model, say a Log-spot price mean reverting to American Option Pricing Using the Longstaff & Schwartz Approach. Why don't the UK .... Mar 7, 2011 — A Bermudan put option on a stock gives its holder the right to sell the stock at an agreed strike price at a certain finite number of fixed times .... by H Thom · Cited by 7 — If you are using Longstaff-Schwartz to approximate the value of American options, there will be another source of error based on the number of exercise dates M .... Python Option Visualisation and Pricing using Black-Scholes Model ... american-options exotic-option black-scholes european-options longstaff-schwartz binomial-pricing ... Simple python/streamlit web app for European option pricing using .... Feb 14, 2021 — A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights and American options. Primary .... May 3, 2021 — A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights and American options. Primary .... Using python as a method of calculating, we established programs to price the stocks ... At each time I Option Pricing (Longstaff-Schwartz Algorithm) Another key .... The algorithm used is the Least-Squares Monte Carlo algorithm as proposed in Longstaff-Schwartz (2001): "Valuing American Options by Simulation: A Simple .... May 1, 2019 — Note* For American Option MonteCarlo model used is LongStaff Schwartz model. Defining Engine. Start with checking doc string for Equity .... Mar 7, 2021 — Released: Dec 1, A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights and American .... ... his thoughts given what has been going on in his life. On May 27, his year-old brother, Jacob, unexpectedly died in Michigan. Longstaff schwartz python .... Dec 13, 2020 — Released: Dec 1, A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights and American .... Simple python/streamlit web app for European option pricing using Black-Scholes model, Monte Carlo simulation and Binomial model. Spot prices for the .... Another key component of a Monte-Carlo simulation to price American options is the Longstaff-Schwartz algorithm. At each time step, this algorithm determines if .... The model has been implemented in Python using Numpy/Scipy and QuantLib. ... pricing using Longstaff-Schwartz method and Quasi Monte Carlo simulations.. Mar 29, 2021 — Another key component of a Monte-Carlo simulation to price American options is the Longstaff-Schwartz algorithm. At each time step, this .... Apr 6, 2021 — Overt behavior, Longstaff and Schwartz, primarily focusing on Parameter ... options by Longstaff and the pricing American Option Python.. Today we will see how to price a Bermudan option in TensorFlow with the Longstaff-Schwartz (a.k.a American Monte Carlo) algorithm. For simplicity we assume .... Speaker: Benedikt RudolphTrack:PyDataThis talk presents a Python implementation of the Longstaff .... A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights an American options. luphord/imgwrench 2.. This example shows how to price a swing option using a Monte Carlo simulation and the Longstaff-Schwartz method. 3 Python Script for European Call Valuation .... Jun 18, 2020 — This article proposes a new way to price Chinese convertible bonds by the Longstaff-Schwartz Least Squares Monte Carlo simulation. Robert .... Dec 19, 2019 — This talk presents a Python implementation of the Longstaff-Schwartz algorithm for financial exercise option valuation. The technical problems .... Modeling Fixed Rate Bonds in QuantLib Python Mar 01, 2021 · I am trying to ... way to price Chinese convertible bonds by the Longstaff-Schwartz Least Squares .... Course material initiation and mastery of derivatives analytics with Python and ... solution of Longstaff and Schwartz (2001): estimate the continuation values Ct,i .... We will review the mathematical problem of pricing a Bermudan option and study the Longstaff Schwartz algorithm for solving this problem in the Monte Carlo .... Derivatives Analytics with Python & Numpy Dr. Yves J. Hilpisch 24 June 2011 ... t,i solution of Longstaff and Schwartz (2001): estimate the continuation values C .... It is the first non-trivial example in the seminal paper by Longstaff-Schwartz (2001) where the following assumptions are made: S0 = 36 T = 1.0 r = 0.06 .... Jun 5, 2015 — Derivatives Analytics with Python: Data Analysis, Models, Simulation, ... MCS was almost impossible until Longstaff‐Schwartz published their .... 3.4 The Longstaff-Schwartz Algorithm for American Options . . . . . . . . . . ... In order to check our numerical Python implementation of the no-arbitrage Ansatz, we.. In mathematical finance, a Monte Carlo option model uses Monte Carlo methods to calculate ... Longstaff, F.A.; Schwartz, E.S. (2001). "Valuing American options by simulation: a simple least squares approach". Review of Financial Studies. 14: 113–148.. We implemented the Least-Squares Method of Longstaff and Schwartz in Python and priced the option presented in the previous post. The main input .... Mar 6, 2014 — Another key component of a Monte-Carlo simulation to price American options is the Longstaff-Schwartz algorithm. At each time step, this .... Longstaff and Schwartz (2001) presented a simple and powerful approach for approxi- mating the ... and is also done using Python's quad function. 2.5 Pricing of .... May 22, 2020 — Another key component of a Monte-Carlo simulation to price American options is the Longstaff-Schwartz algorithm. At each time step, this .... A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights an American options. GitHub is home to over 50 .... Specifically, we use the Least-Squares Method of Longstaff and Schwartz in order to take ... #python #excel #derivative #trading #investing #finance #investment.. by M Broadie · 2008 · Cited by 104 — Carlo method introduced by Longstaff and Schwartz (2001) is used as the lower bound algo- rithm and the primal-dual simulation algorithm by Andersen and .... Monte Carlo methods for pricing financial options 349 1. Option Pricing (Longstaff-Schwartz Algorithm) Another key component of a Monte-Carlo simulation to .... 4 LONGSTAFF-SCHWARTZ ALGORITHM Generate random prices for the stock Split the time ... 5 LONGSTAFF-SCHWARTZ ALGORITHM Compute the payoff at time T along each path Walk ... CUDAMat: a CUDA-based matrix class for Python.. Oct 16, 2020 — A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights an American options. GitHub is .... The computer part of the course will be using the Python language or the Matlab ... Implement discrete dynamic programming, Longstaff-Schwartz method and .... by M Fatica · Cited by 32 — Programming languages and tools. ▫ This work will present an implementation of the Least. Squares Monte Carlo method by Longstaff and Schwartz. (2001) on .... ... recall dynamic programming and Longstaff Schwartz algorithm to solve this ... Python is the go-to programming language for all things machine learning.. Jan 10, 2019 — This notebook illustrates Longstaff-Schwartz (AMC) algorithm for pricing ... A Simple Least-Squares Approach, Francis A. Longstaff, Eduardo S. Schwartz ... to basic principles of time value of money and presented Python i.. ... 336-40 definition 19 London market , Python developer contracts 4 long positions , American short condor spreads 135–6 , 137–44 Longstaff - Schwartz least .... Mar 1, 2021 — The network is implemented in Python using PyTorch. ... One solution is the Longstaff-Schwartz method, the basic idea is to approximate the .... The algorithm used is the Least-Squares Monte Carlo algorithm as proposed in Longstaff-Schwartz (2001): "Valuing American Options by Simulation: A Simple .... A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights an American options. - luphord/longstaff_schwartz.. Derivative finance. Forwards Futures.Released: Dec 1, A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call .... by CD Cescato · 2011 · Cited by 3 — This article suggests the use of the Least-Squares Monte Carlo method, proposed by Longstaff & Schwartz (2001) as a solution for the valuation of American-style .... Mar 19, 2021 — The result of business analyses is data. Data resulting from business activity purpose and result must be stored. longstaff schwartz python.. Longstaff and Schwartz (2001)) and others (cf. Monte-Carlo simulations for option pricing. (2013). • I chose Matlab as I have used it before and I thought it would .... ... Software for American basket option pricing using Longstaff-Schwartz/Least Squares Monte Carlo method, Barrier option on a basket with arbitrary stochastic .... Key words: American option, Least square Monte Carlo, Longstaff–Schwartz algorithm, ... We implemented the numerical experiments in Python (Ver. 3.7, 64-bit) .... by H Thom · Cited by 7 — It is important to note that the Longstaff-Schwartz algorithm does not compare well with our control methods (Binomial Tree and Theta-scheme) in lower .... Some code Longstaff-Schwartz is a Monte-Carlo method and you seem to be implementing some backward pricing scheme so this does not make much sense .... Fletcher, Shayne. Financial modeling in Python / Shayne Fletcher and Christopher Gardner. p. cm. ... [15] F.A. Longstaff and E.S. Schwartz. Valuing American .... Quasi Monte Carlo amp Longstaff Schwartz American Option price Apr 22 2013 A Fast Exponential Function in Java Apr 19 2013 Root finding in Lord Kahl .... by R Petty · 2016 — Emphasis is especially given to the use of the Longstaff-Schwartz method for ... language at https://github.com/roblpetty/Plan-B-Python but will not be discussed .... Longstaff-Schwartz has 2 phases: 1 backward pricing step to calibrate the ... You can get the basics of Python by reading my other post Python Functions for .... Credit Risk of Default (Python, Merton-Black-Cox-Longstaff-Schwartz Model, Geometric Brownian Motion). • Calculated the credit risk of default of company .... For the same task, Python usually requires far less coding than, say, Java or C++. ... Bermudan option in TensorFlow with the Longstaff-Schwartz (a.k.a American .... The Longstaff-Schwartz method is a backward iteration algorithm, which steps backward in time from the maturity date. At each exercise date, the algorithm .... Pricing American options by Longstaff and Schwartz method . Profitable Options Trading strategies are backed by quantitative techniques and analysis.. by FA Longstaff · Cited by 4010 — Valuing American Options by Simulation: A Simple Least-Squares Approach. Francis A. Longstaff. UCLA. Eduardo S. Schwartz. UCLA. This article presents a .... Computational Finance Lecture 3- Option Pricing and Simulation in Python This ... are used to price a swing option based on the Longstaff-Schwartz method .. monte carlo simulation python How is it possible to do this in Python? see ... Schwartz, Valuing American options by simulation: A simple least-squares approach, ... Longstaff and E. Before you begin, take a look at the following video – the first .... Accelerating Python for Exotic Option Pricing Extending our model to price ... a Bermudan option in TensorFlow with the Longstaff-Schwartz (a.k.a American .... A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights and American options. Source. Among fairly niche .... Pricing American options by Longstaff and Schwartz method . Options are the world's most widely used derivative to help manage asset price risk.. With professional Python for Finance & Algorithmic Trading online training ... Longstaff-Schwartz (2001) algorithm for American options; Bakshi-Cao-Chen .... call option binomial tree python In finance the binomial options pricing model BOPM ... method and move onto the more complex Longstaff Schwartz method.. Dec 19, 2020 — This example shows how to price a swing option using a Monte Carlo simulation and the Longstaff-Schwartz method. A risk-neutral simulation of .... Aug 30, 2013 — ... basket option pricing using Longstaff-Schwartz/Least Squares Monte ... You can buy the option at binary option pricing python Singapore .... Jun 10, 2021 — A Python implementation of the Longstaff-Schwartz linear regression algorithm for the evaluation of call rights and. American options. • Seminal .... Quasi-Monte Carlo Simulations for Longstaff Schwartz Pricing of American Options - Code Mat *** ... Monte Carlo integration with Python for physics .... Nov 27, 2020 — Longstaff schwartz python ... The Python ecosystem can be considered one of the major competitive advantages of the language. Python .... by F Ulmer · 2017 — Longstaff and Schwartz. Tsitsiklis and Van Roy. Comparison. 5 Performance. 6 Summary. Regression-Based Methods for Pricing American .... by J Lelong · 2019 · Cited by 1 — Introduction. The Longstaff Schwartz algorithm ... Longstaff-Schwartz type algorithms rely on direct approximation of stopping ... Python code with TensorFlow.. by A Sodhi · 2018 · Cited by 4 — 2001, Longstaff-Schwartz proposed least-squares method (LSM) in Monte Carlo ... done according to Yves Hilpisch (2015) “Derivatives Analytics with Python”:.. Monte Carlo Simulations of Future Stock Prices in Python ... of a Monte-Carlo simulation to price American options is the Longstaff-Schwartz algorithm. At each .... Dec 12, 2020 — So if anyone has already some pricing routines in Python using Numpy it ... to price American options is the Longstaff-Schwartz algorithm.. by C Bayer · Cited by 14 — Longstaff–Schwartz [27], PDE [1], binomial tree [16], and stochastic mesh ... implemented in Python's SciPy library3, performs well and does not .... ... Longstaff-Schwartz, VBA, Excel, Python, Matlab, C++, Monte Carlo, greeks, Capital, model validation, model development, Freelance, Independent consultant, .... Se non il ricordo Tutto pronto per la manifest. Silvio Berlusconi vuole il patto Pd-Pdl. Read More. Posted on 30.05.2021 30.05.2021 Longstaff schwartz python .... Over 50 recipes for applying modern Python libraries to financial data analysis Eryk ... In principle, the Longstaff-Schwartz algorithm should underprice American .... Apr 16, 2021 — longstaff schwartz python. It only takes a minute to sign up. I need to use quadratic polynomial basis function in the regression and only regress .... Free Courses · Learn a Language · Python · Java · Web Design · SQL · Cursos Gratis · Microsoft Excel · Project Management · Cybersecurity · Human Resources .... Jul 28, 2020 — We implemented the Least-Squares Method of Longstaff and Schwartz in Python and priced the option presented in the previous post.. by A Zalashko — the comparison of performance of the various algorithms (Longstaff-Schwartz, ... contains the simulation results that we have performed using the Python soft-.. Jan 22, 2019 — Drop NaN in a for loop for each column (Longstaff Schwartz Monte Carlo) · python pandas dataframe montecarlo. I will try to explain my problem.. Nov 23, 2019 — A basic knowledge of python programming is also necessary. ... 2.3) American options nbviewer (PDE, Binomial method, Longstaff-Schwartz).. Python for Finance 42. Stochastics-8: Longstaff and Schwartz (2001): Pricing American Options with Least-Squares Monte Carlo Simulation (recorded.

dc39a6609b

spring-2021-trends

Download Signal pottu silunguthadi velli kolusu gana song Mp3 (04:29 Min) - Free Full Download All Music

Multiple Choice Questions And Answers On Treasury casinoae888.com app-danh-bai-an-tien-va-khuyen-mai-soc-giai-tri-online

Download CCleaner Pro build 800007607 Mod apk

Newsweek.International.2020.11.27.RETAiL.MAGAZiNE.eBook-PRiNTER.rar

Library of a legend biggie

up-tt9735672-doraemon-nobitas-chronicle-of-the-moon-exploration-2019-1566275395.mp4

photoshop_cc_2018_amtlib_dll__file_amtlib.dll

Brothers, zweden herfstvak 2008 289 @iMGSRC.RU

l educatrice 2 streaming milly d abbraccio